What Is Owner Financing? How It Works, Pros, Cons, and Risks

What is owner financing? It is a way to buy property directly from the seller instead of going through a bank. The seller extends credit to the buyer, who makes monthly payments over an agreed term. In this guide, you will learn exactly how owner financing works, what it costs, who it benefits, and what risks to watch for before signing on the dotted line.

Whether you are a buyer who cannot qualify for a traditional mortgage, a seller looking for monthly income, or an investor eyeing vacant land, owner financing can be a powerful tool. It is also known as seller financing, and it has been used in real estate transactions for decades to bridge the gap between buyers and traditional lending requirements.

What Is Owner Financing?

Owner financing is a real estate transaction in which the seller acts as the lender. Instead of the buyer obtaining a mortgage from a bank or credit union, the two parties negotiate a private loan directly. The buyer makes monthly payments to the seller, who holds a lien on the property until the loan is paid in full.

This arrangement is sometimes called a purchase money mortgage or seller financing. It can apply to houses, commercial buildings, raw land, and other types of real property. The core idea is simple: the seller extends credit, the buyer repays it over time, and ownership either transfers at closing or upon final payment, depending on the contract structure.

Owner financing is especially common in markets where buyers struggle to meet bank lending standards, where properties are unconventional or difficult to appraise, or where sellers want to close quickly without waiting on lender approval timelines.

How Owner Financing Works

The process of owner financing follows a clear sequence. Here is a step-by-step look at how a typical deal comes together:

1. Buyer and seller agree on a sale price, down payment amount, interest rate, repayment term, and balloon payment schedule if applicable.

2. Both parties sign a purchase agreement that outlines all financing terms in writing.

3. A promissory note is drafted. This is the legal document that records the loan amount, interest rate, payment schedule, and consequences for default.

4. Depending on the contract structure, the deed may transfer to the buyer at closing or remain with the seller until the loan is satisfied.

5. A deed of trust or mortgage is recorded with the county to secure the seller’s interest in the property.

6. The buyer begins making monthly payments directly to the seller. Payments typically cover principal and interest, though tax and insurance escrow may or may not be included.

7. At the end of the term, the loan is either paid off in full, refinanced through a traditional lender, or settled with a balloon payment.

Because no bank is involved, the process can close in days rather than weeks. This speed is one of the primary appeals for both buyers and sellers.

Why Buyers Use Owner Financing

Owner financing opens doors that traditional bank lending often closes. Here are the main reasons buyers pursue this arrangement:

• No strict credit score requirements: Sellers can approve buyers based on factors beyond a credit report, including down payment size, income stability, or personal trust.

• Lower barrier to entry: Buyers who are self-employed, recently divorced, or rebuilding credit after hardship often find seller financing more accessible than bank loans.

• Faster closing: Without underwriting delays, appraisals, and lender backlogs, deals can close in a fraction of the time.

• Flexible terms: Interest rates, repayment schedules, and balloon payment dates are all negotiable between the two parties.

• Access to unique properties: Banks often refuse to finance vacant land, fixer-uppers, or rural properties. Sellers of these properties may offer financing to attract buyers who cannot get conventional loans.

• Lower closing costs: Without bank origination fees, points, and other lender charges, buyers often pay less at closing.

Why Sellers Offer Owner Financing

Sellers are not just doing buyers a favor. There are real financial and strategic benefits that make owner financing attractive on the seller’s side as well:

• Faster sale: By removing bank requirements from the equation, sellers reach a larger pool of buyers and close more quickly.

• Monthly income stream: Instead of receiving one lump sum, the seller collects regular payments that function like rental income without the landlord responsibilities.

• Higher sale price: Sellers who offer financing often negotiate a premium price in exchange for the flexibility they are providing.

• Tax advantages: Installment sale reporting can spread capital gains tax over multiple years, potentially reducing the total tax burden.

• Earn interest income: Sellers earn interest on the loan, sometimes at rates higher than they would get from a savings account or CD.

• Broader buyer pool: Sellers can attract buyers who have strong income and a solid down payment but do not qualify for conventional financing.

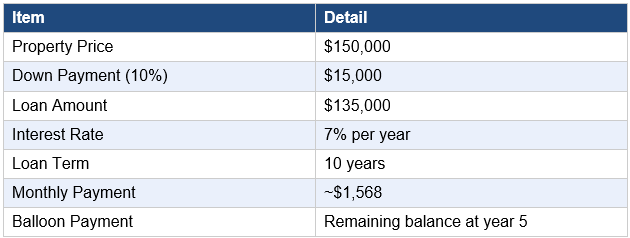

Owner Financing Example

Here is a straightforward example that illustrates how the numbers might look in a real owner financing deal:

In this scenario, the buyer puts 10 percent down and finances the remainder through the seller at a fixed 7 percent interest rate. After five years, the buyer may refinance the remaining balance through a traditional bank. This is a typical structure for owner-financed land deals where the buyer plans to improve the property before qualifying for a conventional mortgage.

Common Owner Financing Structures

Owner financing is not a single contract type. Several legal structures are used, and each has different implications for ownership rights and risk exposure.

Land Contract

Also called a contract for deed, a land contract means the seller retains the legal title to the property until the buyer completes all payments. The buyer holds equitable title and has the right to use the property, but the deed does not transfer until the loan is paid in full. This structure gives the seller strong protection against default but limits the buyer’s ability to refinance or sell the property during the term.

Contract for Deed

A contract for deed is another name for a land contract. The terminology varies by state. In this arrangement, title remains with the seller, and the buyer’s ownership rights depend entirely on remaining current with payments. Defaults can result in forfeiture, meaning the buyer loses all equity and the property reverts to the seller.

Deed of Trust

In a deed of trust arrangement, the property deed transfers to the buyer at closing, and the seller holds a lien secured by a deed of trust. If the buyer defaults, the seller (as beneficiary) can initiate foreclosure through a trustee. This structure provides buyer protection while still securing the seller’s financial interest.

Mortgage Note

A mortgage note is a promissory note secured by a traditional mortgage on the property. The deed transfers to the buyer, and the seller holds the mortgage lien. Foreclosure in case of default follows the standard process, which varies by state and can take months or years. This structure is commonly used in states where mortgage law is well established.

Lease Option

A lease option, also called rent-to-own, allows a buyer to lease the property with the option to purchase it at a predetermined price within a set timeframe. A portion of the monthly rent may apply toward the purchase price. Lease options give buyers time to build credit or save a down payment before committing to a full purchase. However, if the buyer does not exercise the option, they typically forfeit any option premium paid upfront.

Pros and Cons for Buyers

Understanding both sides of the equation helps buyers evaluate whether owner financing is the right move.

Pros for Buyers

• Accessible financing for buyers with poor or nontraditional credit histories

• Flexible terms negotiated directly with the seller

• Faster closing without bank underwriting timelines

• Lower closing costs with no lender fees or points

• Opportunity to buy properties banks will not finance

Cons for Buyers

• Higher interest rates than conventional mortgages in many cases

• Balloon payment risk if the buyer cannot refinance when the term ends

• Limited legal protections compared to bank-regulated mortgage transactions

• Risk of losing all equity if using a land contract structure and defaulting

• Seller may not have clear title, creating title risk for the buyer

Pros and Cons for Sellers

Sellers also carry significant upside and downside in owner financing deals.

Pros for Sellers

• Earn interest income over the loan term

• Close faster with a broader pool of buyers

• Potentially negotiate a higher sale price

• Spread capital gains taxes over multiple years using installment sale treatment

• Retain title protection in land contract structures until fully paid

Cons for Sellers

• Default risk if the buyer stops making payments

• Delayed access to the full sale proceeds

• Foreclosure or forfeiture proceedings can be time-consuming and costly

• Ongoing administrative responsibility for tracking payments and issuing statements

• Property value may decline during the loan term

Owner Financing Risks to Watch For

Both parties take on real risk in an owner financing deal. Here are the most important risks to understand before signing any agreement.

Default Risk: The most common risk for sellers is buyer default. If the buyer stops paying, the seller must pursue legal remedies to recover the property. The process can take months and cost thousands in legal fees.

Balloon Payment Risk: Many owner financing deals include a balloon payment due after a set number of years. If the buyer cannot refinance or pay the balloon at that time, they face default and possible loss of the property.

Title Issues: Buyers should always conduct a title search before closing. If the seller has liens, back taxes, or disputes tied to the property, the buyer could inherit those problems after purchase.

Unclear Contract Terms: Vague or incomplete contracts create serious legal risk. Every term, including interest rate, payment schedule, balloon date, late payment penalties, and default remedies, must be written clearly.

Due-on-Sale Clauses: If the seller has an existing mortgage on the property, the lender may have a due-on-sale clause that requires full repayment when ownership transfers. Buyers and sellers must check for this before structuring any deal.

How to Negotiate an Owner Financing Deal

Negotiating directly with a seller gives both parties more flexibility than a bank allows. Here is how to approach the conversation effectively.

For Buyers

• Start with a strong down payment offer. The more you put down, the more likely the seller is to accept your financing request.

• Research market interest rates so you can propose a fair rate the seller will take seriously.

• Ask for a longer term with a balloon payment option so your monthly payments are manageable while you build equity or credit.

• Request that the deed transfer at closing rather than using a land contract, which gives you more legal protection.

• Avoid agreeing to acceleration clauses that let the seller demand full repayment for minor technical breaches.

For Sellers

• Require a meaningful down payment of at least 10 to 20 percent to reduce your risk exposure.

• Run a background check and verify income before agreeing to terms.

• Set a realistic interest rate that compensates you for the risk and reflects current market conditions.

• Include clear default provisions with specific cure periods.

• Work with a real estate attorney to draft all documents.

Legal Documents You Need

Owner financing requires specific legal documents to protect both parties. Do not skip any of these:

• Promissory Note: The core loan document that spells out the amount borrowed, the interest rate, the repayment schedule, and what happens in case of default.

• Purchase Agreement: The contract that governs the sale of the property, including price, conditions, and closing date.

• Deed of Trust or Land Contract: The security instrument that ties the loan to the property. This is what gives the seller the right to foreclose or reclaim the property if the buyer defaults.

• Warranty Deed or Quitclaim Deed: The document that transfers title, if title transfers at closing.

• Title Report: A search confirming the seller has clear, insurable title free of undisclosed liens.

• Title Insurance: Protects the buyer against title defects discovered after closing.

All documents should be prepared or reviewed by a licensed real estate attorney familiar with the laws in the state where the property is located. Recording the deed of trust or mortgage with the county is essential to protect both parties.

Owner Financing for Vacant Land

Owner financing is especially prevalent in the vacant land market, and for good reason. Banks are reluctant to finance raw land because it produces no income, is harder to appraise, and carries more risk if the borrower defaults. This reluctance creates a natural opportunity for sellers to step in and offer financing directly.

Here is how vacant land owner financing typically differs from house deals:

• Down payments are often higher, ranging from 10 to 30 percent, because lenders perceive more risk in undeveloped land.

• Interest rates on land deals tend to run higher than residential mortgage rates.

• Loan terms are often shorter, with balloon payments due in 3 to 10 years rather than the 15 to 30 year terms common in home loans.

• Land contracts and contracts for deed are more common in land deals, meaning the seller often retains legal title until the buyer pays in full.

• Monthly payments are lower because there is no structure to insure and no property improvements driving up the purchase price.

For buyers of raw land, owner financing can be the only realistic path to ownership. Many sellers of rural acreage, agricultural land, and undeveloped lots are willing to carry the note themselves, especially if they have owned the property for years and want to create an income stream from the sale rather than a one-time payout.

For land investors and flippers, understanding seller financing is a core skill. Many of the best land deals involve motivated sellers who prefer monthly checks over a lump sum, particularly when the tax implications of installment sales work in their favor.

Frequently Asked Questions

What is owner financing?

Owner financing is a real estate arrangement in which the seller provides the loan instead of a bank. The buyer makes monthly payments directly to the seller until the loan is paid off, refinanced, or a balloon payment is due.

Is owner financing the same as seller financing?

Yes. Owner financing and seller financing refer to the same arrangement. Both terms describe a transaction in which the property seller acts as the lender rather than a third-party financial institution.

How does owner financing work?

The buyer and seller negotiate terms directly, including price, interest rate, down payment, and repayment schedule. They sign a promissory note and a security instrument such as a deed of trust or land contract. The buyer makes payments to the seller over the agreed term.

What credit score do you need for owner financing?

There is no standard credit score requirement for owner financing. Each seller sets their own standards. Many sellers will work with buyers who have credit scores below the 620 minimum typically required by conventional lenders, especially if the buyer puts down a strong deposit.

How much down payment is typical for owner financing?

Down payments for owner-financed properties typically range from 10 to 30 percent of the purchase price. Land deals often require more than home deals because of the higher perceived risk. A larger down payment reduces the seller’s exposure and increases the likelihood of approval.

Is owner financing legal?

Yes, owner financing is legal in all 50 states. However, the specific rules governing promissory notes, land contracts, and mortgage documents vary by state. Both parties should work with a licensed real estate attorney to ensure the transaction complies with local law.

What happens if a buyer defaults?

If the buyer defaults, the seller’s remedy depends on the contract structure. In a land contract, the seller may be able to declare forfeiture and reclaim the property. In a deed of trust arrangement, the seller must go through the foreclosure process, which is governed by state law and can take months.

Can you refinance an owner-financed property later?

Yes. Many buyers use owner financing as a bridge while they improve their credit or stabilize their financial situation, then refinance through a traditional lender once they qualify. Balloon payments are often structured to align with a refinancing date.

Is owner financing good for vacant land?

Owner financing is one of the most practical ways to buy vacant land. Banks routinely decline to finance raw land, which makes seller financing the primary option for buyers of rural acreage, agricultural parcels, and undeveloped lots.

What documents are needed for owner financing?

The key documents include a promissory note, a purchase agreement, a deed of trust or land contract, a deed for title transfer if applicable, a title report, and title insurance. All documents should be drafted or reviewed by a qualified real estate attorney.

Final Thoughts on Owner Financing

Owner financing is a flexible, practical, and often underutilized tool in real estate. For buyers who cannot qualify for traditional bank loans, it opens doors that would otherwise stay closed. For sellers, it creates income, attracts a wider audience, and can reduce the immediate tax burden of a lump-sum sale.

The key to a successful owner financing deal is preparation. Understand the structure you are using, whether that is a deed of trust, land contract, or lease option. Get every term in writing. Work with a real estate attorney to draft the promissory note and security instrument. Conduct a thorough title search before closing.

If you are buying or selling vacant land, owner financing is not just a workaround. It is often the best path forward. Banks rarely finance raw land, which makes seller financing the dominant model in land markets across the country.

Ready to explore owner financing for a land deal? Start by understanding the property, running your numbers, and connecting with a real estate attorney who knows the rules in your state. With the right preparation, owner financing can work well for everyone at the table.